Friday, August 03, 2007

Mega-Sales needed to attract Rio Tinto to revives Bakun

The country might have successfully pushed for the construction of one of the largest hydroelectric dam projects in Asia. The Bakun project in Malaysia's Sarawak State was nevertheless hit by several postponements from the period of it being proposed till now, as if there was a curse trying to stop it from completion. It was more than a decade ago when the former premier Mahathir issued the go-ahead, regardless of the concerns on the environmental effects raised and the objection of the relocation of the original settlements within the area.

In the name of development, everything was bull-dozed to  make the mega-project the size of Singapore itself becomes reality. Nothing can stop the decision, and so the Bakun project was started on an area covering 60,000 hectar. All it needs was the 1997-98 Asia Economy Crisis to stop the project, well, at least temporary. And since then the original blue-prints, the main contractors, bulders and others have changed.

make the mega-project the size of Singapore itself becomes reality. Nothing can stop the decision, and so the Bakun project was started on an area covering 60,000 hectar. All it needs was the 1997-98 Asia Economy Crisis to stop the project, well, at least temporary. And since then the original blue-prints, the main contractors, bulders and others have changed.

In late June 2007, the stubborn government seems to have found the pulse to continue the project when Malaysia offered Japan's Sumitomo Corp. (TYO: 8053) a $1.5 billion deal to lay a 700-kilometer long submarine cable which will transmit electricity from Bakun to Peninsular Malaysia despite the fact that the country has excess of 40% of un-used capacity currently.

So, there you go; you have the area the size of Singapore for you to play with by flooding it with waters. The people who stayed on the original lands were forced to settle somewhere else. The economy is back to pre-1997 crisis level (or is it?) and the government needs to spend in order to create business activities. The main contractor is more or less has been finalized and it’s none other than another GLC (government-linked-company) conglomerate Sime Darby Berhad (SIME: stock-code 4197). You have roped in the expertise from Japan to lay the cable and state-owned utility company Tenaga Nasional Berhad (KLSE: TENAGA, stock-code 5347) is surely the buyers of the electricity generated, regardless whether the nation really needs the extra capacity of 2,400 megawatts or not.  But suddenly the government realized they indeed need to build a business justification in order to sell the huge 2,400 megawatts or else the electricity will sit there idling, not that you can put it on the table as one of your dinner’s dishes. If you’re surprise with such methodology, please don’t, as that’s how the country works. The government’s concept is to build the infrastructure and worry about other problems later on as can be seen with most of the city-planning’s methodology. Thus you can see buildings being built up only to realize that the infrastructure such as the roads, severage systems, drainage systems and so on could not cater for future expansion – anyone care to enjoy the fun of having flash floods?

But suddenly the government realized they indeed need to build a business justification in order to sell the huge 2,400 megawatts or else the electricity will sit there idling, not that you can put it on the table as one of your dinner’s dishes. If you’re surprise with such methodology, please don’t, as that’s how the country works. The government’s concept is to build the infrastructure and worry about other problems later on as can be seen with most of the city-planning’s methodology. Thus you can see buildings being built up only to realize that the infrastructure such as the roads, severage systems, drainage systems and so on could not cater for future expansion – anyone care to enjoy the fun of having flash floods?

Earlier StockTube had blogged about the solution to the extra excessive electricity by courting power-hungry industry such as aluminium smelter.There’re couple of major players in the aluminium sector and based on the recent proposal from Rio Tinto (NYSE: RTP,stock) to acquire Canadian aluminum producer Alcan Inc. in a $38.1 billioncash-deal after Alcoa (NYSE: AA, stock) backed off, the Malaysia is talking aggressively trying to court Rio Tinto into Sarawak.

electricity by courting power-hungry industry such as aluminium smelter.There’re couple of major players in the aluminium sector and based on the recent proposal from Rio Tinto (NYSE: RTP,stock) to acquire Canadian aluminum producer Alcan Inc. in a $38.1 billioncash-deal after Alcoa (NYSE: AA, stock) backed off, the Malaysia is talking aggressively trying to court Rio Tinto into Sarawak.

Yesterday, Aug 2, Rio told Reuters that it will sign an agreement next week with its Malaysian partner, Cahya Mata Sarawak Berhad (KLSE: CMSB, stock-code 2852) to pave the way for a feasibility study on a $2 billion aluminium smelter.Cahya Mata is part-owned by the family of Sarawak Chief Minister Abdul Taib Mahmud.

Whether Rio Tinto will proceed to build an aluminium  smelter in Sawarak is yet to be seen, if the earning announcement by Rio yesterday is anything to goes by. Rising costs has cut its profit and the earnings fell to $3.25 billion from $3.8 billion a year ago. Even though the poor result was mainly caused by overruns at Rio Tinto's Argyle diamond mine, the two main commodities that contributing nearly 90% of its earnings are iron ore and copper. Unless the potential profits from the aluminium justify a new smelter, Rio might take its own sweet time to make the decision to expand into Sarawak. Maybe Malaysia can do cheap-sales on the electricity to attract Rio, the same way current “Mega-Sales” is happening throughout Malaysia.

smelter in Sawarak is yet to be seen, if the earning announcement by Rio yesterday is anything to goes by. Rising costs has cut its profit and the earnings fell to $3.25 billion from $3.8 billion a year ago. Even though the poor result was mainly caused by overruns at Rio Tinto's Argyle diamond mine, the two main commodities that contributing nearly 90% of its earnings are iron ore and copper. Unless the potential profits from the aluminium justify a new smelter, Rio might take its own sweet time to make the decision to expand into Sarawak. Maybe Malaysia can do cheap-sales on the electricity to attract Rio, the same way current “Mega-Sales” is happening throughout Malaysia.

For the time being, the other Malaysia government agencies might want to take a look and solve of the problem of “sex-slaves” crying for help trapped inside the Bakun perimeters currently. It’s disturbing to learn that while the gangsters and syndicates are known to supply the women, nothing is being done to rescue them. If you’ve not read this hot story, you can click here to read it. Just because there’re 2,000 workers working within the project doesn’t gives the police the right to justify that the law-enforcers can’t do anything about it.

Other Articles That May Interest You ...

Stumble it!

Stumble it!

Thursday, August 02, 2007

Bad Economy & Crimes Eat into Petrol Stations?

With or without government approval, the 3,200 petrol stations nationwide in Malaysia, including those along highways, will close at 10pm and open at 7am. Most newspaper reported the news and the decision was decided at the annual delegates conference of the Petrol Dealers Association of Malaysia (PDAM) here yesterday.

The justifications for such action: frequent armed robberies, increased security costs, higher wages for workers, low night sales, soaring rentals and electricity bills. To make matter worse, the dealers also want customers who use credit cards to buy petrol to fork out the 1% commission, previously absorbed by the dealers.

“The association’s acting president, Major (Rtd) Wahid Bidin, said the decision was likely to go into effect in two months and added “Last year, every petrol station was robbed at least once … The average collection of only about RM1,000 daily after 10pm did not make it worth their while.”

“However, Federation of Malaysia Consumers Association chief executive T. Indrani said that petrol stations should not be allowed to close early because “The dealers are making profits and, if they were losing, they would not be in business … If they are truly making losses, they should show their income and expense statements to prove that they are making losses.''

While I do not agree with the decision to close the petrol stations at 10pm, I can’t deny the fact that from the business perspective, it’s really not worth the operating cost if what the PDAM claimed is true. City drivers might be able to adapt to the early closure but those operating along highways should remains open.Can you imagine what will happen during the peak season if drivers need to refill gas along the PLUS highway but couldn’t find any petrol stations, not to mention the normal traffic jam even on the pay-highway itself?

While I do not agree with the decision to close the petrol stations at 10pm, I can’t deny the fact that from the business perspective, it’s really not worth the operating cost if what the PDAM claimed is true. City drivers might be able to adapt to the early closure but those operating along highways should remains open.Can you imagine what will happen during the peak season if drivers need to refill gas along the PLUS highway but couldn’t find any petrol stations, not to mention the normal traffic jam even on the pay-highway itself?Unless the dealers can prove they’re making losses, the government should not allow this to

happen. But what if the dealers are right? It might be true that the business is not that rosy though, considering the petrol prices were increased multiple times during the current administration headed by premier Badawi. You might still remember those days when the petrol was at RM1.10 per liter not too long ago and with a stroke of an announcement (the nation’s coffer is drying?) it’s now more than RM1.90 per liter.

happen. But what if the dealers are right? It might be true that the business is not that rosy though, considering the petrol prices were increased multiple times during the current administration headed by premier Badawi. You might still remember those days when the petrol was at RM1.10 per liter not too long ago and with a stroke of an announcement (the nation’s coffer is drying?) it’s now more than RM1.90 per liter.The chain-reaction was that almost all your can think of in your daily expenses has risen – transportation, foods, car-parts and just anything. It’s normal now that car owners drive daily to the nearest LRT (light-rapit-transit) only to park their car and board the LRT. Some resort to cheaper transport alternative – motorcycles, thanks to the forever in-efficient bus transportation.

And due to the government’s policy to import foreign workers especially from Indonesia, the social problems had began to show its’ color – increase in crimes such as arm-robberies, rapes, hijacking, snatch-thefts and anything related to crimes which you can name it. It might makes sense to utilize these foreign cheap labors during the good times but once you’ve a leader who’s not capable to maintain, not to mention increase the nation’s economy expansion, you should get ready to combat battalions of walking zombies terrorizing public’s security.

And due to the government’s policy to import foreign workers especially from Indonesia, the social problems had began to show its’ color – increase in crimes such as arm-robberies, rapes, hijacking, snatch-thefts and anything related to crimes which you can name it. It might makes sense to utilize these foreign cheap labors during the good times but once you’ve a leader who’s not capable to maintain, not to mention increase the nation’s economy expansion, you should get ready to combat battalions of walking zombies terrorizing public’s security.Other Articles That May Interest You …

Moody Says Smaller Deficit, Malaysia Said Otherwise

Moody's Investors Service said Malaysia needs a smaller budget deficit and faster economic growth to earn its first credit rating upgrade since 2004. Standard & Poor's on July 31 raised the outlook on the Southeast Asian nation's foreign currency borrowings to positive from stable, which means the company's first upgrade on Malaysia since 2003 is more likely – reported Bloomberg.

Moody's however said today a stable outlook is more appropriate. Malaysia's government, which has spent more than it earns for nine straight years, plans to maintain a budget deficit this decade to fund a $58 billion development program. Second Finance Minister Nor Mohamed Yakcop in June argued that foreign investment, economic growth and the state's ability to repay debt weren't factored into the nation's credit ratings.

Malaysia's government plans to post a deficit of 3.4 percent or less of gross domestic product until 2010, Yakkop said on July 10. The government expects the economy to expand 6 percent this year after growth of 5.9 percent in 2006.

On July 31th 2007, Standard & Poor's left the rating on Malaysia's foreign currency debt unchanged at A-, the fourth-lowest investment level. Moody's rates Malaysia's foreign currency long-term debt as A3, the equivalent level.

It would be interesting to see how on earth can the government spend less to decrease the budget deficit when the premier Badawi has been promoting one mega-project after another, starting with IDR in southern region of Peninsular Malaysia to NCER in the northern part and now he’s getting ready to launch another one in the eastern part of Kelantan, though on a smaller scale as Kelantan is governed by opposition party.

Looking at the pattern of how Badawi going around the nation promoting new projects one wonders in amusement how could the premier who are known to often fall-asleep even on official functions could suddenly wide awakes giving away all the goodies. The premier could be flying off to Sabah and Sarawak to hand more good news to the locals in the last effort to fish for votes before calling the next general election.

Nevertheless in order to put the chart to shows smaller deficit, the government needs to either increase exports or reduce imports but it’s easier said than done.Artificial figures could do the trick though.

Other Articles That May Interest You …

Wednesday, August 01, 2007

Murdoch’s $60 a share Offer and Fees-Paid Wins

Rupert Murdoch claimed victory today, Wednesday 1st Aug 2007, in his battle to acquire Dow Jones after securing support from enough Bancroft family members to clinch majority backing for his $5.6 billion cash offerfor the owner of The Wall Street Journal. The breakthrough came after nearly four months of often torturous negotiations between the media mogul and the fractious clan of heirs to a family which has controlled the leading US financial newspaper for more than a century.

Mr Murdoch overcame objections from inside and outside the family that his hands-on editorial style and tabloid newspaper sensibility would tarnish the Journal's reputation for high editorial standards and independence. The 76-year-old mogul, who has in the past 50 years built News Corp from a small Australian newspaper group into a global media giant, has had his eye on the Journal for at least a decade.

The Bancrofts control 64 per cent of Dow Jones's voting shares, held through a complex series of privately-held trusts. More than half the family votes, representing more than 30 per cent of Dow Jones's overall voting shares, are needed for News Corp to be confident that its offer will be voted through by a majority of the company's shareholders. A turning point came on Tuesday after a Bancroft family trust holding around 9 per cent of Dow Jones's voting shares dropped its push for a higher price from Mr Murdoch. Instead, it agreed to back the deal after receiving assurances that the family's fees would be paid as part of the deal.

The Bancrofts control 64 per cent of Dow Jones's voting shares, held through a complex series of privately-held trusts. More than half the family votes, representing more than 30 per cent of Dow Jones's overall voting shares, are needed for News Corp to be confident that its offer will be voted through by a majority of the company's shareholders. A turning point came on Tuesday after a Bancroft family trust holding around 9 per cent of Dow Jones's voting shares dropped its push for a higher price from Mr Murdoch. Instead, it agreed to back the deal after receiving assurances that the family's fees would be paid as part of the deal.Murdoch's $60 a share offer, a 65 per cent premium to Dow Jones' share price before news of News Corp's interest emerged carried the day after he agreed to a last-minute deal sweetener by helping to cover millions of dollars of legal and advisory costs incurred by the Bancroft family. By adding it to a stable of media properties that run from tabloids such as The Sun in London and the New York Post, to Fox News Channel and MySpace, Mr Murdoch cements his position as the dominant force in global media.

Based on Murdoch’s vision for Dow Jones to establish The Journal as the rival to The Times in setting the daily news agenda of the country, there is little doubt that he will directly aim at luring both readers and advertising away from The New York Times and The Financial Times, The Journal’s closest rivals. His strategy will probably include aggressively undercutting advertising and investing heavily in editorial content – reported New York Times.

When he repurchased The New York Post in 1993, he focused on raising the paper’s circulation by cutting the cover price of the paper several times and handing out copies free. “If he hadn’t come in, there wouldn’t have been a New York Post,” said Jerry Fragetti, senior vice president for media and operations at Newspaper National Network, who worked as chief financial officer of The Post in the 1980s and as an executive for the News Corporation in the early 1990s.

After IDR now NCER – Segregating Pies

Just what happens to the highly marketed and the buzzling of IDR (Iskandar Development Region), the first mega-project initiated by Malaysia’s premier Badawi which is suppose to be another clone of Hong Kong or Dubai spanning over 20-year whileattracting 105 billion dollars?

Before anything has taken off in a scale which can instill confidence that IDR is not a fantasy but a real thing, the premier today ambitiously launched the Northern Corridor Economic Region (NCER) project which will see the transformation of Penang into a modern, vibrant city and a major logistics and transportation hub. The NCER is said to be the bullet to turn Penang into the “Gateway to the Northern Corridor”. Excuse me but aren’t Penang has been the “gateway” to the northern Malaysia all this while? Either this is another nice marketing strategy to further segregate projects to the ruling party’s linked companies (or cronies) or the Chief Minister of Penang has done a damn bad job in maintaining, not to mention developing, the status of Penang as the northern gateway.

![]()

Everyone knows the main company which benefits the most from IDR is the UEM World Berhad (KLSE:UEMWRLD, stock-code 1775), a construction firm linked to ruling UMNO party and the one which has huge lands located within IDR. So, you shouldn’t be surprise if the NCER is another way to give the other pieces of pie toMalaysian Rresources Corporation Berhad (KLSE:MRCB, stock-code 1651), another GLC (government-linked-company) and Equine Capital Berhad (a close business associate of Badawi). Did I hear someone said General Election is around the corner?

Everyone knows the main company which benefits the most from IDR is the UEM World Berhad (KLSE:UEMWRLD, stock-code 1775), a construction firm linked to ruling UMNO party and the one which has huge lands located within IDR. So, you shouldn’t be surprise if the NCER is another way to give the other pieces of pie toMalaysian Rresources Corporation Berhad (KLSE:MRCB, stock-code 1651), another GLC (government-linked-company) and Equine Capital Berhad (a close business associate of Badawi). Did I hear someone said General Election is around the corner?

Anyway, compare to IDR, NCER seems to have a stronger and clearer blueprint, at least on the paper. To start the ball-rolling, at least a China company has been secured to finance and build the Penang second bridge. Among some of the sub-projects within the high-level blue-print for NCER are:

- Penang Sentral integrated transport hub – a RM2 billion modern transportation and logistics hub to transform Butterworth into a modern metropolitan area, covers 557,418 square metres. The hub will integrate rail, ferry, monorail and land transport modes – the came concept as KL Sentral. Winner - MRCB

- Penang Global City Centre – a RM18bil project to transform Penang Turf Club into a modern city center which will have international exhibition and conference centre, shopping complexes, two five-star hotels, commercial and residential properties, a state-of-the-art cultural centre and a 10.5ha park. Winner – Equine Capital Berhad (KLSE: EQUINE, stock-code 1147). Does this sound like KLCC to you, both also on the land of turf club with the same concept?

- Second Penang Bridge – a RM2.7 billion bridge connecting mainland and Penang which will be the South-East Asia’s longest bridge. Expected to be complete by 2011, it will be built under a joint-venture between UEM Builders Bhd and China Harbour Engineering Co Ltd.

- Pulau Jerejak premier medical tourism centre

- Penang-Butterworth fast ferry

- Penang Port expansion

- Bayan Lepas Airport expansion

- Penang 37km Monorail

- Swettenham Pier redevelopment

- Micro-Electronics Centre of Excellence

- Hospitality college

- Khazanah Nasional Bhd regional office

In June MRCB was awarded a contract by Pelaburan Hartanah to build houses and apartments with a combined gross development value (GDV) of RM500mil on three sites on Penang Island. Analysts expect MRCB to secure additional projects in the state such as the construction of the proposed monorail and Penang Outer Ring Road (PORR).

While MRCB might have proven itself with the KL Sentral project (though I’ll reserve the comment on the successfulness of it), it’s mind-boggling to note that Equine Capital Berhad was given the RM18 billion project considering it only registered RM131 million revenue for the financial year 2006 as compare to RM140 million in 2007. The net profit was a double-digit of RM17 million (2006) and RM31 million (2005) respectively. So can Equine take the risk of a project more than 10 times its’ annual revenue? But then the boss of Equine, Patrick Lim, probably carries more weight than anyone else – at least in the Malaysia’s political world if not corporate world.

While MRCB might have proven itself with the KL Sentral project (though I’ll reserve the comment on the successfulness of it), it’s mind-boggling to note that Equine Capital Berhad was given the RM18 billion project considering it only registered RM131 million revenue for the financial year 2006 as compare to RM140 million in 2007. The net profit was a double-digit of RM17 million (2006) and RM31 million (2005) respectively. So can Equine take the risk of a project more than 10 times its’ annual revenue? But then the boss of Equine, Patrick Lim, probably carries more weight than anyone else – at least in the Malaysia’s political world if not corporate world.

Neverthless it’s definitely the people’s hope that all these billions of dollars would put to full good use and development to benefits everyone rather than another wasteful mega-project which only benefits a few cronies as accustomed to the Malaysia’s ruling party’s business policy.

Other Articles That May Interest You …

Tuesday, July 31, 2007

STEMLIFE Skyrocket without anyone notice

It was merely about two-weeks ago when StockTube wrote about TMC Life Sciences Bhd (KLSE: TMCLIFE, stock-code 0101) stock any justify why you should own it in your portfolio. Yes I know the stock has not move yet (you’re really impatient when come to stocks investing, aren’t you?), in fact it has consolidated from the peak to current RM1.38 per share, well above the support of RM1.24. Isn’t this a good level for you to accumulate, you greedy investor (or rather punter?) who always thinks of making fast money overnight?

Well, this post is not to talk about TMC Life but rather on StemLife Berhad(KLSE: STEMLFE, stock-code 0137). Between the two devils, StemLife’s stock obviously performs better. Just to refresh, it was about two-weeks ago on the same article, I was nagging about how I should not have sold my positions in StemLife, even though I’m still holding a very small amount of shares as of now. On the date of that article being written, the stock price of StemLife was about RM4.00+ per share. Can you please go and take a look at the price now?

But if you have found StockTube’s blog and read the article on why you should invest in TMC Life and StemLife stock back in Jan 2007 when it was trading at about RM1.00 per share, you would have gained a whopping 400 percent in profitif you had just follow the recommendation blindly. If only life is so predictable, it would be a wonderful world, won’t it?

Anyway, looking at the momentum and technical analysis, you would noticeStemLife has been trading within a narrow but uptrend range without failsince it broke out from the resistance of RM2.60 per share in 21st May 2007. The stock is trading at RM 5.75 per share at the time of writing. Will it reaches RM7.00 or even RM8.00 per share? With the amount of 5 cents on every next bid after RM5.00 per share, it’s a matter of time before the target is reached, provided the trading range is not broken.

Anyway, looking at the momentum and technical analysis, you would noticeStemLife has been trading within a narrow but uptrend range without failsince it broke out from the resistance of RM2.60 per share in 21st May 2007. The stock is trading at RM 5.75 per share at the time of writing. Will it reaches RM7.00 or even RM8.00 per share? With the amount of 5 cents on every next bid after RM5.00 per share, it’s a matter of time before the target is reached, provided the trading range is not broken.

Having said that, aren’t StemLife expensive at the current share price? You bet, it’s obvious the stock is being “fried” but considering the stock has Goldman Sachs (8.85% stake) and JP Morgan (4% stake) in its shareholders list (as of Mar 2007), it’s not that difficult to convince others the stock could goes up further. The latest would be Capital Group International Inc. which acquired 5.27 percent stakeon 4th July 2007. Furthermore StemLife is the main player in the stem-cell storage in town with TMC Life set to kick-in sometime in September 2007 to give StemLife a run for some money. It was said that come 2008, the number of players would increase to 7 (seven) in the stem-cell banking business giving more competition.![]() Regardless whether the StemLife is frying the stock to make fast bucks or knowing in advance that it might be “acquired”soon (please don’t drop your jaw in surprise *grin*), the shares will continue to attract a small of followers who are laughing all the way to the bank. I mentioned small followers because the daily volume is negligible. I won’t complaint a word if you start to buy StemLife and help push the price higher. Of course I would hope the stock will skyrocket to RM10.00 per share but then I should accumulate in stages on TMC Life, don’t you think so?

Regardless whether the StemLife is frying the stock to make fast bucks or knowing in advance that it might be “acquired”soon (please don’t drop your jaw in surprise *grin*), the shares will continue to attract a small of followers who are laughing all the way to the bank. I mentioned small followers because the daily volume is negligible. I won’t complaint a word if you start to buy StemLife and help push the price higher. Of course I would hope the stock will skyrocket to RM10.00 per share but then I should accumulate in stages on TMC Life, don’t you think so?

Other Articles That May Interest You …

Monday, July 30, 2007

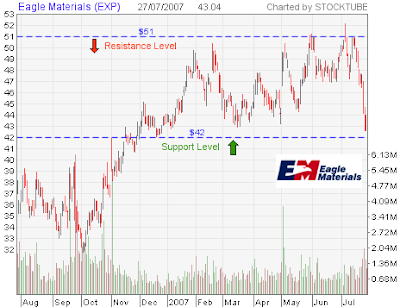

Could the Eagle Fly Against the Weak Housing?

Eagle Materials Inc. (NYSE: EXP, stock) is set to announce its earning today, Monday 30th July 2007, after market close. Eagle Materials Inc. is a manufacturer of basic building materials, including gypsum wallboard, cement, gypsum and non-gypsum paperboard and concrete and aggregates. The CompanyGÇÖs primary businesses are the manufacture and distribution of gypsum wallboard and the manufacture and sale of cement. Gypsum wallboard is distributed throughout the United States with particular emphasis in the geographic markets nearest to its production facilities. It sells cement in four regional markets.

Rating Indicators for EXP:

Sales, Income & Growth - For the past 12-months, Eagle Materials registered $922.4 Million in sales versus the industry’s $14,313 Million. Income amounted to $203.00 Million against the industry’s $1,334 Million. While Eagle’s 12-months sales growth is at 7.30% the income growth is 25.90% (the same industry sector sales growth is at 12.00% and income growth of -0.20%).

Profitability & Financial Health – For the past 12-months, net profit margin is in the region of 22.0%. Eagle Materials has a debt/equity ratio of 0.37 compare to industry’s ratio of 0.62.

Stock Resistance & Support Level – The resistance is at 44.88 (200-day moving average) while the first level support is at 31.76 (52-week low)

Risks – The shares are heavily sold by financial institutions.

The struggling housing sector has taken its’ toll on the housing stocks such as Beazer Homes, D.R. Horton and Pulte Homes. Related stocks in building suppliers which supply cements such as Eagle Materials is affected as well. But compare to direct home suppliers, cements could be diverted elsewhere. Furthermore the share price of Eagle has consolidated from its peak at $51 per share to current $43.50 per share, nearing its support of $42.00.

The struggling housing sector has taken its’ toll on the housing stocks such as Beazer Homes, D.R. Horton and Pulte Homes. Related stocks in building suppliers which supply cements such as Eagle Materials is affected as well. But compare to direct home suppliers, cements could be diverted elsewhere. Furthermore the share price of Eagle has consolidated from its peak at $51 per share to current $43.50 per share, nearing its support of $42.00.

Based on its’ track record in beating earning estimate, it could be the most valuable bullet in investing its option or stock. We have not heard much news on the merger of cement players since May when a German cement company said it’s considering to buy over Hanson PLC.

The War between Bloggers and Government Peaks

It’s very disturbing to note the war between Malaysian bloggers (political bloggers to be specific) and the UMNO, the main party component of the ruling Malaysian Government has started to peaks and potentially couldspread into other categories of bloggers – financial, personal, mum-and-dad or even food and recipe blogs.

Almost all printed and electronic licensed medias in Malaysia are controlled, one way or another by the ruling Government which has been in the power since the 1957 Independence. People were said to be fed with positive news only by these controlled medias but everything changes when the “blog” (or web log) was created and gains momentum. Thanks to the technology, people who know the basic internet surfing can now turn to read the other side of the stories.

UMNO, of which the ministers are mostly aged and moulded into walking zombies who will only follows the instruction from the highest person who walks the corridor of powers, have been taken by surprise of the popularity of certain blogs. One similarity that hit all the famous bloggers in Malaysia which command tens of thousands to millions of views per day is that almost all of them are being charged (or going to be charged), one way or another by the government.

UMNO, of which the ministers are mostly aged and moulded into walking zombies who will only follows the instruction from the highest person who walks the corridor of powers, have been taken by surprise of the popularity of certain blogs. One similarity that hit all the famous bloggers in Malaysia which command tens of thousands to millions of views per day is that almost all of them are being charged (or going to be charged), one way or another by the government.

First it was Jeff Ooi (his blog http://www.jeffooi.com/), Ahirudin Attan a.k.a. Rocky (his bloghttp://rockybru.blogspot.com/) and then the webmaster of opposition party PKR, a Harvard-graduate Nathaniel Tan(his arrest). But none of the above attracts the wide-publicity or the cyber-supports as compare to Raja Petra Kamarudin whose critical articles in his blog,http://www.malaysia-today.net/, invited the UMNO to make a police report. The prominent political writer Raja Petra was then interrogated by police for 8 hours for sedition following complaints that articles on his blog belittled Islam and tried to stir racial tension in the multiethnic nation.

First it was Jeff Ooi (his blog http://www.jeffooi.com/), Ahirudin Attan a.k.a. Rocky (his bloghttp://rockybru.blogspot.com/) and then the webmaster of opposition party PKR, a Harvard-graduate Nathaniel Tan(his arrest). But none of the above attracts the wide-publicity or the cyber-supports as compare to Raja Petra Kamarudin whose critical articles in his blog,http://www.malaysia-today.net/, invited the UMNO to make a police report. The prominent political writer Raja Petra was then interrogated by police for 8 hours for sedition following complaints that articles on his blog belittled Islam and tried to stir racial tension in the multiethnic nation.

Authorities have not made clear which of Raja Petra's articles were allegedly seditious but most readers suspected that the government started the war againts Raja Petra (and others?) after his article (read here) on allegations against Inspector General of Police (IGP) Musa Hassan. The Attorney General was surprisingly fast in passing the verdict to clear the IGP and thus government leaders used it as the reason to calls for bloggers to be controlled.

Authorities have not made clear which of Raja Petra's articles were allegedly seditious but most readers suspected that the government started the war againts Raja Petra (and others?) after his article (read here) on allegations against Inspector General of Police (IGP) Musa Hassan. The Attorney General was surprisingly fast in passing the verdict to clear the IGP and thus government leaders used it as the reason to calls for bloggers to be controlled.Nazri, another minister sparked concerns over online freedom last week after he said the government was drafting new laws for bloggers and would not hesitate to use the Internal Security Act, which allows for detention without trial, against bloggers who insult Islam or stir sensitive topics.

Khairy Jamaluddin, deputy youth leader of the ruling Malay party and the prime minister's son-in-law called for legal action taken against bloggers who spread lies and slander. "There are no laws in the cyberworld except for the law of the jungle. As such, action must be taken so that the monkeys behave," Khairy was quoted as saying by Bernama.

And today, the government continues the war when Information Minister Zainuddin told the newspaper that the public should be wise in identifying the websites of goblok (Indonesian slang for “stupid”) bloggers, who are willing to be tools of others to destroy the nation. He added that these writers do not have an Asian mentality but lean towards a Western thinking because they were educated overseas.

In his latest salvo, Raja Petra wrote an interesting article titled Raja Petra seditious? Hogwash! after his previous mild article on See you in hell Muhamad son of Muhamad. Raja Petra claimed and pointed out a few IDs that belonged to the 25 UMNO cyber-troopers recruited by UMNO as the persons who actually left the sensitive comments in his blog (read the article a comedy of errors). Malaysia Today is so influence that Raja Petra claimed there was DOS attack launched against the blog.

Regardless of which party wins the war ultimately, the government is definitely wrong and subject to the laughing stock of other countries if it indeed tries to blackout all the other bloggers. As most of the ministers are not IT-literate, you can only expect the worst in any rules, regulations or laws drafted and proposed by them to control the bloggers. However I’m very interested to know how the government plans to block “permanently” those blogs hosted by Google’s Blogger’s platform or blogs hosted overseas. At this moment, the government can only block (such as the case of Malaysia Today) blogs within Malaysia only. Even then there’s a workaround to it unless the Internet Service Providers are instructed to press the button to “power-off” all the equipments.

Regardless of which party wins the war ultimately, the government is definitely wrong and subject to the laughing stock of other countries if it indeed tries to blackout all the other bloggers. As most of the ministers are not IT-literate, you can only expect the worst in any rules, regulations or laws drafted and proposed by them to control the bloggers. However I’m very interested to know how the government plans to block “permanently” those blogs hosted by Google’s Blogger’s platform or blogs hosted overseas. At this moment, the government can only block (such as the case of Malaysia Today) blogs within Malaysia only. Even then there’s a workaround to it unless the Internet Service Providers are instructed to press the button to “power-off” all the equipments.

It’s time for the ruling government to learn the rope of cyber-blogging and accept the fact that bloggers are here to stay. It’s sad to read that while the U.S. Democrats are taking the debate to a higher level of YouTube, Malaysia’s government is still struggling to learn the basic of e-mail and surfing (readhere), let alone blogging. If you practice good governance (the same way in corporate governance), nobody will cares about Raja Petra’s blog but if you’ve barrels of worms planted all over the place, then any Tom, Dick and Harry’s article would make you jump up in the middle of your sleep.

Sunday, July 29, 2007

GreenPacket – Light at the End of the Tunnel?

The last entry StockTube touched on Green Packet Berhad (KLSE:GPACKET, stock-code 0082) was on June 25th, 2007 when the stock plunged the second time since it broke the support of RM4.80 per share. I’ve wrote about what StockTube see from the RSI and Stochastic technical reading. The post also highlighted what could be the concerns or problems haunting Green Packet stock back then. StockTube also mentioned that from the perspective of technical and fundamental, the stock will surely rebound from the support of RM4.00 per share – and it did rebound beautifully. You can read more about the post here at Relook at GreenPacket Stock - Problem or Opportunity?

So I hope those who have confidence in the stock had made some money from the rebounce after the stock touched the support of RM4.00 per share on 25th June 2007. And if you care to relook at the chart of Green Packet it soared and hit the resistance of $4.80 per share before plunges back thereafter. Between RM4.00 and RM4.80, that’s 20 percent of good and easy money to be made, only if you traded within the range.

July 13th 2007 was the date that changed the landscape of Green Packet stock’s pattern; it was also the day of bonus issue and share consolidation. The chart that you’re seeing on this post has taken that into consideration – I’ve since re-map the support and resistance level.

July 13th 2007 was the date that changed the landscape of Green Packet stock’s pattern; it was also the day of bonus issue and share consolidation. The chart that you’re seeing on this post has taken that into consideration – I’ve since re-map the support and resistance level.What’s the Technical Lookout of GPacket?

Since there’s no change in the fundamentals of Green Packet, we can only analyze from the technical perspective of the stock. The concerns are still the high receivables which might prompt investors in dumping the shares recently. But whether the stock’s plunge has anything to do with the shares restructuring or thepiece of important news which will be revealed at the later part of this post (so, continue reading) is still up to everyone’s guess.

StockTube does not apply hundreds of technical reading to confuse and scare the shits out of readers as it is assumed most readers are not technical-savvy. To make money investing stocks or trading option should be fun and not boring and complicated to the extent of costing your good night sleeps.

Referring to the chart that has been blown-up above, you can see how volume plays a very significant but almost ignored role in giving you hint of what’s actually happened or about to happen. On both occasions that saw the stock rebound when it touched the support of RM5.40 (RM4.00 before shares restructuring), it were followed or had accumulation signals prior. These accumulations by buyers indicate that investors (outsiders or insiders) are ready to bargain hunt on such scenario as the stock was seen to be attractive.

Referring to the chart that has been blown-up above, you can see how volume plays a very significant but almost ignored role in giving you hint of what’s actually happened or about to happen. On both occasions that saw the stock rebound when it touched the support of RM5.40 (RM4.00 before shares restructuring), it were followed or had accumulation signals prior. These accumulations by buyers indicate that investors (outsiders or insiders) are ready to bargain hunt on such scenario as the stock was seen to be attractive.However, if you look at the consolidation after the bonus issue and shares consolidation, there were obvious sign of sellers’ distribution. Why investors didn’t see this as an attractive level to scope the shares are beyond normal investors’ basic understanding. You should take such price-volume-action with a pinch of salt and not scratching your head till you become bald. There’re many reasons to this and if you’ve trade U.S. stock market long enough, such pattern is normal. It could be the investors “knew” some bad things are going to happen and these investors are not you or me. They’re the insiders or professionals. So am I saying insiders are selling or insiders are feeding crucial info to others to sell or refuse to buy? Your guess is the same as mine.

Often “invinsible hands” are playing the advance game of buying or selling before normal investors can even blink their eyes. And by the look at the distribution volume, the chart is telling you the stock could have more falling to go before testing the support of RM3.75 or even RM3.30. Don’t you like to have the choice of shorting the stock now *evil grin*?

Angel to the Rescue

Now, I mentioned there’s a piece of news that is rather important to the development of GPacket’s stock action next week onwards. If you care to check the filing in the Kuala Lumpur Stock Exchange, you would notice that there’s one very crucial new shareholder emerged in GPacket. It’s none other than Goldman Sachs Group, the global investment group which has a capitalization of a whopping USD78 Billion.

Goldman Sachs acquired 455,275 shares on 18th July 2007 and another 1,000,000

It’s not easy to make US$10 Billion income on revenue of over US$76 Billion in the last 12 months of operation. So you got to give this new shareholder some respects with the decision to invest in GPacket. And since GPacket’s shares were acquired at the price of lower than RM5.40 per share (based on the date of purchase), it only makes sense to conclude that Goldman Sachs has confident the stock price will goes up above the acquisition price in order for it to make money before exit.

Hence, could it be the Goldman Sachs is the light at the tunnel for Green Packet? It could be the sunshine that would make you tons of money; it could also be the main reason why the stock plunges since then. One way or another, you’ve to accept the rules of the stocks investing game.

Other Articles That May Interest You …

Friday, July 27, 2007

China’s Syndrome – ICBC Stock Exposure

Of late, there has been great interest in foreign-stock Call Warrants among the Malaysian stocks investors, simply because the local growth stories could be boring or seems to be ending. Couple with the fact that the Composite Index is trading at the range of 1,300+ without the ability to bypass the 1,400 mark, the audience just got inpatient – people wants to see stocks move up so that they can make money.

So, when the Call Warrants which were based on foreign-stocks hit the bourse,people just scrambled into the counter without knowing what it is, resulting in the warrants being pushed up in 2-digit gains within the listing day. Little did these punters know what are the factors affecting the Call Warrants’ stock performance.

To refresh everyone, there’re basically two factors which will enable you to make money if you plan to play with this new Call Warrants. First if the respective foreign share price goes up, then the call-warrants will be in-the-money (a term which I hijacked from option trading). Second, if the foreign currency (of the original foreign-stock) appreciates against Malaysian Ringgit, then you’re in luck because the value of the Call-Warrant will have higher value.

The two investment banks which dominate the foreign-stock Call Warrants locally are CIMB (Commerce International Merchant Bankers, an investment bank of Bumiputra-Commerce Holdings Berhad (KLSE: COMMERZ, stock-code 1023)) andOSK. While CIMB likes to issue the Call Warrants in European-style, OSK prefers the American-style and there’re definitely differences between both styles, mind you.

Tired of CIMB, let’s talk about OSK which had issued some American-style foreign-stock Call Warrants. Among them are:

- PetroChina Company Limited (PETROCH-C1, stock-code 0500C1)

- China Mobile Limited (CHMOBIL-C1, stock-code 0501C1)

- Industrial And Commercial Bank Of China Limited (ICBC-C1, stock-code 0502C1)

Due to the request from one of StockTube readers, let’s focus only on ICBC Call Warrant at this particular moment. ICBC-C1 was listed in local stock market on 5th June 2007 with approximately 50 million of floating shares. To summarize the important data an investor should know:

- Expiry-date – 29th February 2008 (9 months)

- Issue Price – RM0.12 per share

- Exercise / Conversion Price – HKD 4.38

- Exercise / Conversion Ration – 2 Call-Warrants for 1 ICBC-share

How Big is ICBC?

Industrial And Commercial Bank Of China Limited (HKG: stock 1398) is the mainland’s largest lender which was founded as a limited company on Jan 1st 1984. As of June 2006, it had assets of over RMB 7,000 billion (US$893 billion) with 18,764 outlets including 106 overseas branches and over 2.5 million corporate customers plus 150 million individual customers. ICBC was listed both in Hong Kong Stock Exchange and Shanghai Stock Exchange on 27th Oct 2006.

Already, ICBC overtook Citigroup as the new world’s biggest bank early of the week when its stocks’ surged to give it a market capitalization of $254 Billion versus Citigroup’s $251 Billion. However in terms of profitability, Citigroup is still the leader with income four times larger than its nearest competitor. But while Citigroup is only trading at 11 times its 2007 EPS (earnings per share), ICBC is trading at the hot and dangerous multiple of 28 times level. ICBC benefits mostly from the appreciation of Yuan against the Dollar.

ICBC recently was reportedly said it might announce more than 50 per cent growth in net profit for the first six months of the year 2007, as compare to a net profit of 25.14 billion yuan in the first half of 2006

Technical and Fundamental Analysis

A glance at the chart of ICBC since it went public will tell you that the immediate resistance is at HK$ 5.00 with the first level support at HK$ 4.40 and second level support at HK$ 4.00. The HK$ 4.40 became the support level after it was breached sometime in the middle of June 2007. So you should know how to trade this stock with this piece of information, if you’re trading the ICBC shares itself in Hong Kong Stock Exchange.

As highlighted above, ICBC is the equivalent of Malaysia’s Malayan Banking Berhad (KLSE: MAYBANK, stock-code 1155) so I’ll skip the portion of the fundamental. Suffice to say ICBC would not become a penny stock unless the whole China’s economy collapsed. Nevertheless, the stock is trading at an alarming high multiple of 28 times and this should be your main risk.

As highlighted above, ICBC is the equivalent of Malaysia’s Malayan Banking Berhad (KLSE: MAYBANK, stock-code 1155) so I’ll skip the portion of the fundamental. Suffice to say ICBC would not become a penny stock unless the whole China’s economy collapsed. Nevertheless, the stock is trading at an alarming high multiple of 28 times and this should be your main risk.

Should You Invest in ICBC Call Warrant?

As of today, 27th July 2007 (2:50pm trading time) ICBC is trading at HK$ 4.70 per share while ICBC-C1 (Call Warrant on KLSE) is trading at RM 0.135 per share. If you decide to convert the Call Warrant to ICBC share (or mother share), it will be:

- (2 x RM 0.135) + (4.38 / 2) = RM 2.46 (assuming 1 RM = 2 HK$)

- Translate into 2.46 x 2 = HK$ 4.92 per share

- Which means you’re paying a premium of 4.68 % over its’ actual value.

But the premium of HK$ 0.22 (RM 0.11) is a small and attractive value to payfor the remaining time-value as the expiration is on 29th Feb 2008. If you compare to most Malaysia’s warrants which are way out of money, ICBC-C1 is indeed very attractive.

Supposing you’re greedy and would like to maximize your profit and you believe HK$ 4.40 will be a strong support and you intend to invest when it hit this level, nothing more and nothing less. So I’m sure you can work the conversion back the same way to see what’s the ICBC-C1 price that you should go in, can’t you?

Supposing you’re greedy and would like to maximize your profit and you believe HK$ 4.40 will be a strong support and you intend to invest when it hit this level, nothing more and nothing less. So I’m sure you can work the conversion back the same way to see what’s the ICBC-C1 price that you should go in, can’t you?

Other Articles That May Interest You ...

AvalonBay provides Apartment and Stock Dividend

When people talked about money, somehow the conversation topics couldn’t run too far away from stock investing and property or real-estate investment. StockTube have blogged about Mah Sing Group Berhad and E & O Property Development Berhad as the favorite stocks in property sector. Now, let’s fly out of the country and travel a couple of thousands miles towards U.S.

Avalon Bay is actually a REIT (real estate investment trust) company which focused on developing, operating and owning apartment communities in the Northeast, Mid-Atlantic, Midwest, Pacific Northwest, Northern California and Southern California regions of the United States. As of March 31, 2007, AvalonBay owned about 171 apartment communities containing 49,402 apartment homes in ten states in U.S.

Through the Investor Relations segment, Avalon Bay claimed that its average annual Funds from Operations (FFO) per share growth and dividend growth have exceeded the industry average. Considering Avalon’s Compound Annual Growth Rate of 19.5%, it is definitely a set of impressive data out-beating the S&P500 and Nasdaq’s growth. Since the company went public back in 1994 (trades on the New York Stock Exchange and under the ticker symbol "AVB"), AvalonBay Communities, Inc. has consistently paid dividends each year since then.

So, if you happen to think about owning an apartment in California, Massachusetts, Washington, New York or elsewhere in U.S., you probably might want to give Avalon a thought.

Dow Jones Plunges 300 - Expect Regional to Drop

Wall Street suffered its second-biggest plunge of the year Thursday, extending its weeks-long streak of volatility after disappointing home sales figures added to investors' increasing uneasiness about the mortgage and corporate lending markets. The Dow Jones industrials briefly fell more than 300 points (as of trading hour at 2pm), while Treasury yields plunged as investors moved money from stocks to bonds.

Investors who had been able to shrug off concerns about subprime mortgage lending problems and a more difficult environment for corporate borrowing were clearly worried once again. The Dow's drop is the biggest since it plummeted 416 points on Feb. 27 after a nearly 10 percent decline in Chinese stock markets.

The anxiety on Thursday increased after the Commerce Department reported thatsales of new homes fell 6.6 percent last month to a seasonally adjusted annual rate of 834,000 units, more than triple what had been expected and the largest percentage drop since sales fell by 12.7 percent in January.

Thursday's trading was the latest in a series of frenetic sessions over the past month - many accompanied by triple-digit swings in the Dow - as investors sold on worries about the subprime fallout or bought on optimism that there wouldn't be any widespread problems caused by mortgage failures. Many analysts have described the back-and-forth trading as overwrought and based more on gut emotion than careful consideration of market and economic fundamentals.

So, expect the regional markets including Malaysia to open lower when the Friday stock market resumes trading for the last day of the week. The week market definitely pulled down the performance of Apple Inc as most of the indexes are in red. Apple would have performs better if not for the plunge.

Thursday, July 26, 2007

China Mobile the Actual Rescuer for TIME?

Who would have guess that Malaysia loss-making Time DotCom Berhad (TIMECOM: stock-code 5031) had quietly sneaked out of the country desperately looking for life-partner? Everyone thought this hopeless stock would either partner with a local telco company (DIGI.com or Telekom) or be bailed out by the government. Hence, Time Engineering (KLSE:TIME, stock-code 4456) together with Time DotCom’s stocks price were bid up when the rumor hit the street that Hong Kong-listed China Mobile Ltd is interested in Time Engineering which holds 40.68 percent stake in Time DotCom.

However, Second Finance Minister Nor Mohamed Yakcop said today the Malaysian government is not aware of the interest by China Mobile. As usual, you’ve to take the statement by Yakcop with a pinch of salt as he seldom issues concreate statements. China Mobile(HKG: 0941) could indeed be talking to Time Engineering and unless China Mobile denies it, the rumor and possibility of Time DotCom finally being rescued will continues.

However, Second Finance Minister Nor Mohamed Yakcop said today the Malaysian government is not aware of the interest by China Mobile. As usual, you’ve to take the statement by Yakcop with a pinch of salt as he seldom issues concreate statements. China Mobile(HKG: 0941) could indeed be talking to Time Engineering and unless China Mobile denies it, the rumor and possibility of Time DotCom finally being rescued will continues.With more than RM850 million in debts, Time is dying and if the country’s coffer allows it, the government would definitely not think twice about bailing it out, the same way billions of public money was being used to do so during previous premier Mahathir’s rule, not to mention Time is one of the important business entity within UMNO, the biggest party component in the current ruling government.

StockTube would not be surprised should the acquisition

goes through if the recent contract to provide soft-loan, design and build the second multi-billion Penang bridge by a Chinese-based company is used as the gauge of Malaysian Government’s approach towards Malaysia-China business relationship. While former premier adopted pro-Japan policy, current Badawi could be adopting pro-China policy which makes sense looking at how the emerging giant is giving even U.S. a headache on the huge trade inbalance in favor of China.

goes through if the recent contract to provide soft-loan, design and build the second multi-billion Penang bridge by a Chinese-based company is used as the gauge of Malaysian Government’s approach towards Malaysia-China business relationship. While former premier adopted pro-Japan policy, current Badawi could be adopting pro-China policy which makes sense looking at how the emerging giant is giving even U.S. a headache on the huge trade inbalance in favor of China.Nevertheless StockTube would be interested to know the final stake that Time is willing to let go – definitely China Mobile will not accept anything less than a controlling stake, would it?

Other Articles That May Interest You …

APPLE Jumped, StockTube Jumped

You could be wondering why StockTube was not updated since I blogged about APPLE Should Beats Earning but Other Number Counts, that’s one day ago. In actual fact, I was re-researching Apple stock and could only find optimistic data that point to Apple will definitely beats earning. I’ve to admit I was quite nervous if Apple will join Google’s party. After the earning announcement, I jumped in joy, not too much on the news that it indeed beaten the earning estimate again but because the new set of numbers indicating the iPhone sold is double of what reported by AT&T Inc. (NYSE: T, stock) earlier.

Apple Inc.'s fiscal third-quarter profit soared more than 73 percent and it sold 270,000 iPhones in the first two days on the market. That’s the headline which sent Apple stock up by more than 9 percent ($12.92 in extended trading hour), enough to send short-sellers to cover their shorts when the trading starts on Thursday. Although the iPhone figure didn’t contribute to the earning announced, it simply means Apple future earning can depends on iPhone to bring in cash into the coffers.

As reported by AP and most of the financial news, it’s a well-known fact that Steve “always” issues a conservative outlook that fell short of Wall Street's expectations during the earning announcement. So most investors just smiled and sent the stock skyrocket at the same time.

As reported by AP and most of the financial news, it’s a well-known fact that Steve “always” issues a conservative outlook that fell short of Wall Street's expectations during the earning announcement. So most investors just smiled and sent the stock skyrocket at the same time.

For the quarter ended June 30, Apple's profit rose to $818 million, or 92 cents per share, up from $472 million, or 54 cents a share in the year-ago quarter – easily beats the estimate of $0.72 per share by Thompson Financial. Sales grew to $5.41 billion from $4.37 billion last year against estimate of $5.28 billion. The conservative figures from Apple itself were projected earnings of 66 cents per share on quarterly sales of $5.1 billion.

“Steve Jobs said “We're thrilled to report the highest June quarter revenue and profit in Apple's history, along with the highest quarterly Mac sales ever … iPhone is off to a great start … We hope to sell our one-millionth iPhone by the end of its first full quarter of sales … and our new product pipeline is very strong”.

The company said it shipped a record 1.76 million Macs, up 33 percent from the year-ago period, accounting for $2.5 billion, or more than 60 percent of the quarter's revenues. Unit sales of iPods increased by 21 percent from last year to 9.8 million and generated $1.57 billion in revenue. You should wait and see the numbers when Apple announce the iPhone sales in the next subsequent quarter.

The reason for the discrepancy between Apple's and AT&T's numbers on iPhone sales was unclear and the only reason raised at this moment is the service activation problems. There was initially some disappointment in the 270,000 iPhone units, but as people realized the gross margins came in at 37 percent, they were very encouraged by the profitability of the company as can be seen with the Apple stock price’s reaction during the extended hours.

The reason for the discrepancy between Apple's and AT&T's numbers on iPhone sales was unclear and the only reason raised at this moment is the service activation problems. There was initially some disappointment in the 270,000 iPhone units, but as people realized the gross margins came in at 37 percent, they were very encouraged by the profitability of the company as can be seen with the Apple stock price’s reaction during the extended hours. Before Apple's results were announced, its shares rosed $2.37, or 1.8 percent, to close at $137.26. Then in a heavy-volume trading after hours, shares fell as much as 6 percent before they rose more than 9 percent to $150.18. What can you learn from these 3 lines of information? DO NOT trade during extended hours, period. Extended hours are not designed for small investors to trade the stocks (option trading stops completely at 4:00pm) in the hope of making money. You should work as a professional investor in the U.S. to know what I meant. These market makers made transactions faster than you can blink your eyes during this hour, trading against the opposite side of the market makers. So, you small boys or girls should just grab a cup of coffee and sit there watching the show.

# TIP: Do not trade stocks during extended hours, it’s not for you.

Other Articles That May Interest You ...

Tuesday, July 24, 2007

APPLE Should Beats Earning but Other Number Counts

Top U.S. telecommunications service provider AT&T Inc. (NYSE: T, stock) said on Tuesday quarterly profit and revenue rose, helped by growth in wireless and Internet subscribers. AT&T, which began selling Apple's iPhone on June 29, however said it activated 146,000 iPhone subscribers in the first two days of the launch with more than 40 percent of those subscribers were new customers.

The data immediately sent stock price of Apple Inc.’s (Nasdaq: AAPL, stock) plunge 4 percent (off $5.70 to $138.02) this morning’s trading before recovered to minus $4.00 or down by 2.85 percent (as of 10:30am Tuesday). The 146,000 iPhone sales were well below analyst estimates.

Apple Inc. is set to announce its’ earning tomorrow, Wednesday 25th July, 2007 after market closed. So would Steve be able to announce another round of earning which will beat the estimate $0.72 per share? It has to if Apple wishes to see today’s disappointed figure of iPhone sales and the share’s drop be compensated and set a dynamic and uptrend or possibly gap-up.

If the investors smell any earning figures which do not looks impressive enough, it could be punished a second time. And the second time of punishment would not be a nice view to look at, that’s for sure. Nevertheless going by the normal conservative figure given by Steve as usual, Apple is on the high probable of beating the estimate. It’s a question of whether the set of numbers are impressive enough for analysts to say the current stock price is trading at the lower range (and substantially raise their targets).

Trading at P/E (price to earning ratio) of 45.50, Apple’s stock price is not cheap. It’s even higher than Google Inc. which is trading at 43.60 multiple of its earning. Not an easy decision to make if you should long or short the stock, don’t you think? Well, depending on how long is your investment for Apple, you might want to long it if you’re optimistic the iPhone numbers will eventually go above analysts’ estimate.

Dividend Yield Stocks (Part 1) – Berjaya Sports Toto

There’ve been numerous requests from readers of StockTube on recommendation on stocks which give away good “dividend yield”. This type of stock is also one of the favorites among the long-term investors who see it as a better alternative to banks’ fix-term-deposit saving or even the EPF’s (Employees Provident Fund) pathetic annual dividend. The latter is applicable for retirees who are planning to grow their hard-earned savings.

Basically stocks which can provide good and “consistent” dividend pay-out are normally defensive stocks, meaning comes rain or shine the stocks will still pay you dividend. I’ve previously blogged about two stocks (upon request from a loyal reader) which consistently pay relatively good dividends. The reader couldn’t make the decision as to which stock to invest, so StockTube published the article onWhich Stock to Invest - GENTING or Public Bank? back in end of May 2007 to summarize the comparison.

StockTube New Mini Project

StockTube will starts (in no particular order) to publish several articles on stocks that provide “Good and Consistent Dividend Yield”, one stock at a time with more fundamental and technical information. I’ll neither commit on the time-period of the next subsequent article nor would I commit on the number of stocks which fit the topic. I’ll just let the flow takes its course. Let’s kick-start with one of my favorites, Berjaya Sports Toto Berhad (KLSE: BJTOTO, stock-code 1562).

Sports Toto Malaysia Sdn Bhd was incorporated in 1969 by the Government of Malaysia, was privatised on 1st August 1985 and thus separated its’ status quo as a state-owned gaming enterprise. Sports Toto is currently a wholly-owned subsidiary Berjaya Sports Toto Berhad which is listed on the Bursa Malaysia or Kuala Lumpur Stock Exchange.

Sports Toto is the sole national lotto operator with over 680 outlets throughout Malaysia and offers a variety of games – digit-type games (namely, 4D, 5D and 6D) and lotto-type games (namely, Toto 6/42 Jackpot, Super Toto 6/49 and Mega Toto 6/52). The Company has total staff strength of more than 450 working at its head office in Kuala Lumpur and branches throughout Malaysia, and over 1,500 staff employed by agents of the Company.

The Man behind Berjaya Sports Toto

If you do not know yet, Berjaya Sports Toto Berhad is part of Berjaya Corporation which is owned  by none other than Tan Sri Dato’ Seri Vincent Tan Chee Yioun. Vincent used to be on the corporate front-page during the former premier Mahathir period. He was said to be one of the Chinese corporate cronies of Mahathir and he was well-known within the circular of stocks investors in the 1990s for the infamous “rights issue” and “bonus issue”, so much so that Vincent Tan’s listed companies consists of billions of floated shares – one of the highest around.

by none other than Tan Sri Dato’ Seri Vincent Tan Chee Yioun. Vincent used to be on the corporate front-page during the former premier Mahathir period. He was said to be one of the Chinese corporate cronies of Mahathir and he was well-known within the circular of stocks investors in the 1990s for the infamous “rights issue” and “bonus issue”, so much so that Vincent Tan’s listed companies consists of billions of floated shares – one of the highest around.

As the “King of bonus and rights issue”, it wasn’t a surprise that the share prices of his Berjaya companies rarely hit above 2-digit figure due to enormous floating shares in the market, with the exception of Berjaya Sports Toto. Due to the nature of the business, Berjaya Sports Toto is undoubtly the ultimate cash-cow for Berjaya Corporation and Vincent Tan as the largest shareholder.

Sports Toto’s Fundamental

Fundamentally, Berjaya Sports Toto, just like any other gaming (or gambling) stocks is a defensive stock. Despite the regulation which only allows certain days of the week for punters to bet on their luck, all the outlets continue to attract customers. Since 1997 (and prior to that) the revenue has never once registered below RM 1 Billion figure. During the 1997 Asia Economy Crisis the company saw a jump in revenue to breach the RM2 Billion mark – a proof that people will bet even more during the difficult time.

Profit has grown from a mere RM343.7 Million in 1997 to RM571.9 Million in financial year ended 2006. The earnings per share (EPS) were rather on the yo-yo trend mainly due to the inter-company restructuring but shareholders will definitely see 2-digit of earnings per share as registered since 1997.

Profit has grown from a mere RM343.7 Million in 1997 to RM571.9 Million in financial year ended 2006. The earnings per share (EPS) were rather on the yo-yo trend mainly due to the inter-company restructuring but shareholders will definitely see 2-digit of earnings per share as registered since 1997. The company reserve however has grown from 1997 from RM109 Million to RM1.2 Billion in 2002 only to be reduced to RM366 Million in 2004 before picking up to RM463 Million in 2006.

The company reserve however has grown from 1997 from RM109 Million to RM1.2 Billion in 2002 only to be reduced to RM366 Million in 2004 before picking up to RM463 Million in 2006.

Technical Analysis on the Stock

Looking at the 3-year chart, Sports Toto has since rebound from the boring RM3.00 per share to above RM4.00 per share. Due to the consistent and expected result of the gaming stocks revenue, the share price rarely jumps (or drops) beyond imagination. The first level support is at RM4.90 per share while the second level support is at the strong RM4.30 per share. The resistance is at the RM5.50 per share level. Since the stock breached the support of RM4.90 about a month ago (June 19th, 2007 to be exact) it could be too early to tell if the immediate resistance (RM5.50) or support (RM4.90) will holds.

The first level support is at RM4.90 per share while the second level support is at the strong RM4.30 per share. The resistance is at the RM5.50 per share level. Since the stock breached the support of RM4.90 about a month ago (June 19th, 2007 to be exact) it could be too early to tell if the immediate resistance (RM5.50) or support (RM4.90) will holds.

However, if you analyze the volume distribution and accumulation pattern, the technical chart seems to comply with the rules, meaning the opportunity to buywhen it consolidate to the support of RM4.90 nears.

Dividend Analysis

A glimpse on the gross dividend per share summary chart will shows that the Berjaya Sports Toto is a stock to own if you’re looking at the rare 2-digit return on investment. It wasn’t so attractive pre-2005 with a single-digit of dividend returns. For the financial ended 2005, it declared a total RM0.45 per share of dividend while the attractiveness increased in 2006 when it declared RM0.51 per share. This is about 10 percent annual return, not a bad figure for dividend hunters. It is estimated the company will declare the same $0.51 per share, if not higher, for the financial year ended 2007’s dividend payout. The latest dividend declared is the fourth interim dividend of 7.5 sen per share (less 27% income tax) with the expiration-date on Aug 15th, 2007 and the payment-date on Aug 30th, 2007. This 7.5 sen is however was said to be lower than the expected 10.5 sen by certain analysts.

It is estimated the company will declare the same $0.51 per share, if not higher, for the financial year ended 2007’s dividend payout. The latest dividend declared is the fourth interim dividend of 7.5 sen per share (less 27% income tax) with the expiration-date on Aug 15th, 2007 and the payment-date on Aug 30th, 2007. This 7.5 sen is however was said to be lower than the expected 10.5 sen by certain analysts.

Should you go in now?

This is perhaps the most popular question I received in my mailbox. While I can give you a 100-pages analysis, I simply cannot tell the future if some external factors beyond my control will take a particular stock out of the trading range as pictured in the technical chart. What I can tell is if everything goes by the book, the best time to go in is at RM4.90 or slightly lower, provided you are lucky enough.

On June 23, Berjaya Sports Toto launched the Mega 6/52 Jackpot with a minimum RM2 million jackpot. This gave its daily lotto revenues a 25% boost and with three lotto games in its belt, it is believed the stock will continue to performs.

Having said that, if you happen to see an abnormal high volume or selling, please raise the red-flag. This stock is perhaps another good example of how you can make money trading within the range. Stay tune for the next part of investing dividend yield stocks to make money out of it.

Monday, July 23, 2007

Could Crane’s Stock Price Be Lifted-Up?

Crane Co. (NYSE: CR, stock) is set to announce its earning today, July 23rd, 2007 after market close. Crane Co. (Crane) is a diversified manufacturer of engineered industrial products. The Company operates in five segments: Aerospace & Electronics, Engineered Materials, Merchandising Systems, Fluid Handling and Controls.

The Aerospace & Electronics segment consists of two groups: the Aerospace Group and the Electronics Group. The Engineered Materials segment consists of Crane Composites and Polyflon. The Merchandising Systems segment consists of two groups: Vending Solutions and Payment Solutions. The Fluid Handling segment consists of the Crane Valve Group (Valve Group), Crane Pumps & Systems and Crane Supply. The Controls segment consists of Barksdale, Azonix, Dynalco, Crane Environmental and Crane Wireless Monitoring Solutions. During the year ended December 31, 2006, Crane acquired Dixie-Narco Inc., Noble Composites, Inc. and Telequip Corporation. In 2006, it acquired certain assets of Automatic Products International and substantially all of the assets of CashCode Co. Inc.

Rating Indicators for CR:

- Wall Street consensus : 0.78

- StockScouter rating : 8 / 10

- Whisper Number for this stock : N/A

- Schaeffer rating for this stock : 7 / 10

- Power Rating : 6 / 10

- Insider Trading (last 52 weeks) : ($5.00 M)

- Zacks Analysts Rating: Hold

- Option Trading: Dec 2007 45.00 Call

- Implied Volatility (IV) for Sep 2007 $45.00 Strike : 25.92%

Sales, Income & Growth - For the past 12-months, Cranel registered $2.34 Billion in sales versus the industry’s $87.31 Billion. Income amounted to $172.13 Million against the industry’s $10,478 Million. While Crane’s 12-months sales growth is at 14.40% the income growth is 16.70% (the same industry sector sales growth is at 46.20% and income growth of 24.70%).

Sales, Income & Growth - For the past 12-months, Cranel registered $2.34 Billion in sales versus the industry’s $87.31 Billion. Income amounted to $172.13 Million against the industry’s $10,478 Million. While Crane’s 12-months sales growth is at 14.40% the income growth is 16.70% (the same industry sector sales growth is at 46.20% and income growth of 24.70%).

Profitability & Financial Health – For the past 12-months, net profit margin is in the region of 7.4%. Crane has a debt/equity ratio of 0.44 compare to industry’s ratio of 2.13.

Stock Resistance & Support Level – The resistance is at 44.98 (52-week high) while the first level support is at 44.59 (50-day moving average)

Risks – The ratio of Crane's price-to-earnings multiple (17.00) to its five-year growth rate is above the average of all stocks within the same sector. The volume is relatively low so you might not be able to get a good price on the option.

Another stock which is on StockTube radar is Waters Corporation (NYSE: WAT,stock) which is expected to announce its earning on Tuesday, 24th July, 2007 before market open. However you need to have lots of time-value on Waters as it normally trend-up rather late.

Major Crackdown on Malaysia Political Bloggers Started?

In yet another breaking news (how StockTube wish there’s a similar CNN “Breaking News” in Malaysia), theStar reported that UMNO (the main party of the current ruling government) has lodged a police report againstMalaysiaToday for carrying a series of comments and remarks that it deemed as insulting the Yang di-Pertuan Agong, degrading Islam and as inciting hatred and violence in Malaysia's multi-racial society.

Party information chief Tan Sri Muhammad Muhammad Taib lodged the report at 12.57pm at Tun H.S. Lee police station here Monday. He said the comments and remarks, consisting of criminal elements and inciting religious and racial sentiments which could affect the country’s security, were carried by the blog on July 11.

The report was lodged under Section 121 (B) and Section 123 of the Penal Code, Section 4 of the Sedition Act 1948 and Section 263 and Section 266 of the Communications and Multimedia Act 1998.

The report was lodged under Section 121 (B) and Section 123 of the Penal Code, Section 4 of the Sedition Act 1948 and Section 263 and Section 266 of the Communications and Multimedia Act 1998.

Could this mark the start of a major crackdown on political bloggers who wrote the other side of the stories as compare to the traditional pro-government news? A visit to MalaysiaToday today often could not get through, most probably due to high traffic to the famous news portal which attracts tens of thousands of visitors per day. However the author was said to know in advance that his portal will be closed down on Monday and he will be charged and arrested.

What could be the reason for the possible charge or arrest of Raja Petra Kamarudin, the author of MalaysiaToday? Could it be due to this article which has many theories or could it be earlier articles which highlighted what could be thegreatest exposure since the creation of George Lucas’s Star Wars or Steven Spielberg’s Jaws? Though many reasons could be presented as to why certain bloggers were being pulled into court, the latest crackdown on Raja Petra could spell that the General Election is indeed around the corner and the government is not taking any chance which will deny it the overwhelming winning ticket.

Time DotCom – to Acquire or be Acquired?